By Briahnna Brown

Less than 50 percent of Black households own their homes, compared with just over 75 percent of white households, according to a new report from the National Association of Real Estate Brokers.

Vanessa Perry, associate dean for faculty and research and professor of marketing for the George Washington University School of Business, was the primary author for the report released Tuesday. The report analyzes the current state of Black homeownership, market opportunities for Black homebuyers and recommendations for public policy interventions to help alleviate housing disparities.

Amid the financial devastation from the coronavirus pandemic, which disproportionally impacts Black people, and calls for racial justice around the world, now is a critical time to analyze the systemic barriers to economic equality that Black people in America face, Dr. Perry said. Policy interventions like the CARES Act have established a number of protections for home owners, she said but at this time there is no way to tell how long those protections will last.

Dr. Perry spoke with GW Today about the state of Black homeownership and what policymakers can do to be prepared to address this issue before the end of the pandemic.

Q: What do we already knew about Black homeownership, and why are the rates so low?

A: So, the homeownership rate for the Black people is 47 percent. It actually went up 5 percentage points between 2019 and early 2020 thanks to the strong economy and low interest rate environment. Obviously, we're concerned about the pandemic's effect on homeownership going forward, but the homeownership rate now is approximately the same as it was in 1968, when the Fair Housing Act was passed. And so, if you go back over 52 years, most people would argue that there's been a lot of progress that Black Americans have made in terms of education and occupational opportunities. There's been many, many advances in the state of Black America over the last 52 years, but the homeownership rate is the same. You’ve got to wonder what that is about.

In this report, we have argued that these disparities have occurred because of historical discrimination and the cumulative effects of this disadvantage over time. Black people tend to have lower wealth, and are concentrated in racially segregated areas in large cities on the coasts. These are the reasons that are usually cited for why the homeownership rate is so low relative to the 76 percent that it currently is for white households. What this report argues is that it's important that we acknowledge the role of systemic racism and discrimination and redlining that have led to these circumstances, and that public policy needs to address these underlying problems directly.

Fifty-two years wasn't that long ago, and some of these explicit redlining practices persisted up through the 1970s. Now in the digital age, there are many other ways that this disadvantage manifests itself. The homeownership industry—which is multiple industries combined such as real estate, participants in the housing finance system, including investors in the secondary mortgage market, etc.—has taken at various points in time what it considers to be very serious steps towards increasing Black homeownership opportunities, but it hasn’t been able to really make any real gains. That is because the system as it is currently set up basically penalizes people for circumstances that they inherited. That is why the homeownership rate hasn't really changed. The system that we currently have in place has certain barriers, certain challenges that until those are overcome, we won't see any major changes in homeownership.

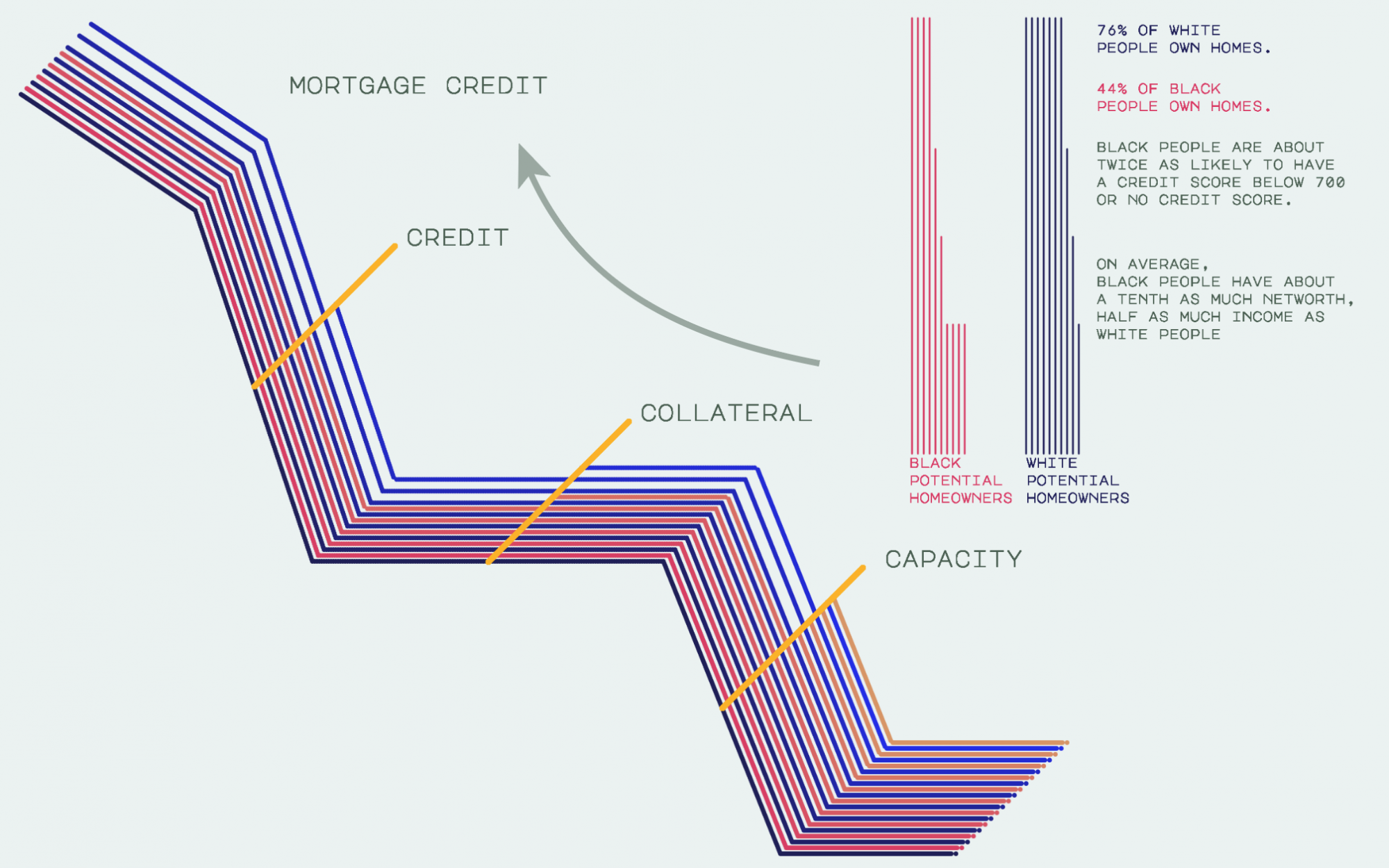

Figure: Black Borrowers Face Challenges in Access to Mortgage Credit and Homeownership

Q: Could you expand on what you mean by “the system penalizes people”?

A: So, in one part of the report, some of my colleagues do a real deep dive in analyzing why it is that Black households pay more for homeownership. It actually costs more for Black people to be homeowners: They pay, on average, higher interest rates, higher insurance rates, have lower house price appreciation and lower home values. So homeownership actually costs more both in the short run and the long run, and the gains from homeownership for Black homeowners are lower, so the returns on home ownership are lower for Black homeowners. There's a big difference in the benefits that Black people have been able to derive from homeownership.

The other reason I call it a penalty is because, let's just say, for example, you grew up in a family that could not afford to pay for your college education, and so you do what many American young college students do: You take out student loans. While student loan debt balances are significantly higher for Black college students, Black college students are also more likely to have to leave college before graduation, there are also differences in the kinds of colleges that Black students often attend and the ability of these institutions to be able to provide financial aid resources without the student loans.

As a Black graduate, you will have on average a significantly larger student loan burden that may very well set you back, because those loans would need to be repaid on a regular basis. This affects both your ability to qualify for a mortgage, and it affects the amount of cash that you have available and reduces the amount of money that you could otherwise save. So, the person in this example is at a disadvantage when it comes to becoming a homeowner, compared to someone who has smaller or no student loan obligation.

Many people who are in college now, their parents and certainly their grandparents may have been precluded from being homeowners because of redlining and segregation and some really poorly-put-together policies in the part of the Federal Housing Administration (FHA). They were often forced to live in low-value neighborhoods where lots of loan defaults and foreclosures occurred which ended up becoming distressed neighborhoods. Homeowners weren't able to build home equity the way that others were as a result of these federal policies that existed less than 50 years ago. And so, for those reasons they don't have the equity, which becomes wealth to use to be able to fund their children's college education, so the children end up with student loans. It becomes this kind of compounding or what we call cumulative disadvantage.

There are some studies I've seen that estimate that the millennial generation is entering home ownership something like nine years later than prior generations, largely because of student loan obligations. And so that's why I frame it as a penalty system; it penalizes people or shuts them out for circumstances beyond their control.

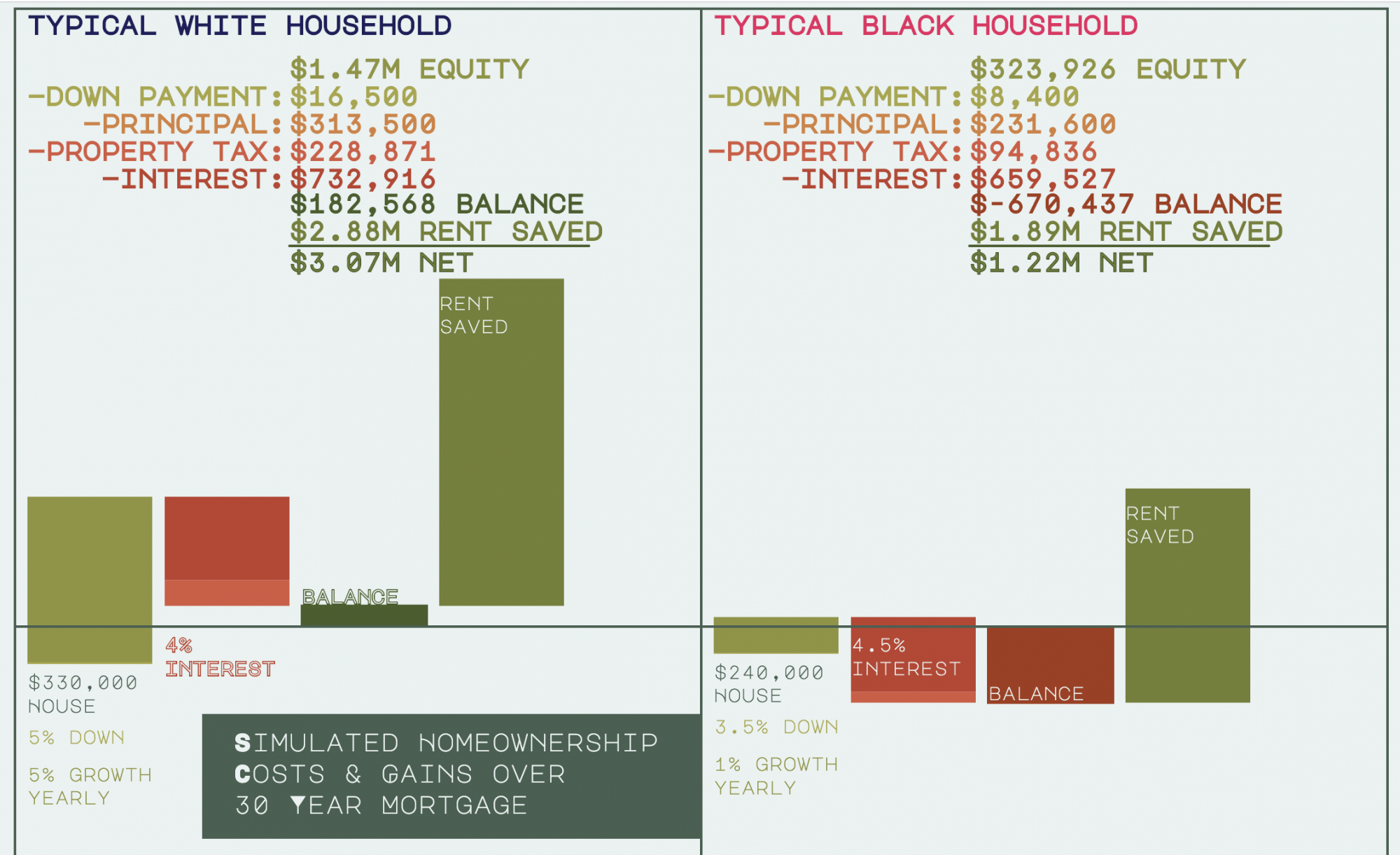

Figure: Disparities in Homeownership and Access to Credit Contribute to Cumulative Wealth Inequality

Q: What were some of the key findings from the report, and was there anything that you were surprised to see when you were collecting this information?

A: I think the most surprising thing is the finding about how much more Black homeowners pay, and how much they're charged for risk-based pricing policies in the mortgage market. Risk-based pricing is not new, but basically that means you pay a higher interest rate because your financial circumstances make you have a higher risk of defaulting on your mortgage. We've known what these factors are, and we've known that they affect Black home buyers differently for a long time, but it wasn't until working on this report that I actually saw how much that costs.

Black people, on average, pay something like $743 more per year in interest costs. Why? Because Black home buyers tend to be more likely to take out FHA or other government-insured loans that are often more expensive, and they pay more in mortgage insurance costs. Because tax assessment rates tend to exceed the rates of home appreciation in Black neighborhoods, property taxes also tend to be higher in a lot of cases, and so when you add all of that up over the life of a typical mortgage it's something like an extra $13,000. Over time, that ends up being $67,000 in lost retirement savings. That's a lot of money. That makes a huge difference. If you think about this sort of intergenerational effects of that, it really is significant.

Some of the other things that I wasn't aware of had to do with the disparities in home values because of segregation. Cities in this country are very highly segregated by race, and the difference between the home values in minority neighborhoods versus home values in predominantly white neighborhoods is stark. That has sort of profound implications, not just on sort of the financial gains from home equity but also on differential access to education, health care and employment opportunities. Many other things are tied to segregation versus integration, and and changes haven’t happened the way that I think policymakers in the ’60s and ’70s who were really focused on this thought that they would.

Q: What are the some of the things that policymakers and regulators who want to improve housing equality should be trying to do about this?

A: I would love to see people think about policies from the lens of cumulative disadvantage, and address those issues that that have occurred as a result of Black home buyers not being able to qualify for mortgages and not being able to access homeownership opportunities because of circumstances that were out of their control. That will result in a different set of policy prescriptions.

We've been tweaking policies and guidelines for 50 years, and certainly since the advent of automated underwriting in the late 1990s early 2000s, which we thought was going to revolutionize homeownership opportunities because now we could eliminate a lot of the mortgage discrimination that existed when people were going into brick-and-mortar lending institutions and getting loans. We thought we could automate our way into better opportunities, and that hasn't really happened.

Why? Because for one, discrimination occurs in all sorts of subtle ways that aren't necessarily obvious, but beyond that, just setting overt discrimination aside for a second, the real issue is perhaps things that happened one or two or three generations ago to Black people prevent them from being able to catch up to similarly-situated white people in the United States.

Some of those kinds of public policies include things like student loan forgiveness, such as in programs like the Employer Participation Act which allows employers to provide down payment assistance for homebuyers, restoring consumer protections and enforcement that are already on the books like enhancements to the Fair Housing Act that requires that lenders evaluate their policies for a negative and disparate impact on minority borrowers; or Affirmatively Furthering Fair Housing (AFFH), which was eliminated by the U.S. Department of Housing and Urban Development, recently, under the Trump administration, which was requiring state and local governments to take steps to make sure that fair housing protections occurred on that level. So, those kinds of things actually will address the underlying issues, which are systemic and historical racism and discrimination.