By Briahnna Brown

While financial literacy levels are low for all U.S. adults, a January 2020 survey found that women correctly answered 49 percent of personal finance index questions compared to men who correctly answered 56 percent.

A new report from the Global Financial Literacy Excellence Center (GFLEC) at the George Washington University School of Business and the TIAA Institute highlights existing disparities in financial literacy among different groups in the U.S., said Annamaria Lusardi, GFLEC founder and academic director and University Professor at GW. This data is critical in finding what gaps to pinpoint for half of the population, Dr. Lusardi said, and knowing that the disparities are compounded for women of color is especially important given the disparate health impacts of the COVID-19 pandemic.

“The crisis give us an opportunity to reimagine the future, and we cannot go back to the “normal” before the pandemic because that normal was not good enough. The time has come to focus on women, Dr. Lusardi said. . “It is time that we invest in women, in making them more financially resilient.”

Dr. Lusardi spoke with GW Today about the findings in the report and what they mean for women’s financial preparedness amid this economic crisis:

Q: What has previous research told us about women’s financial literacy?

A: Over time we have done a lot of research on women, and I have to say that it's only when we started doing international comparisons that we discovered there is a gender difference in financial literacy both in the United States and around the world. When we look at financial literacy, we see over and over that women know less than men, and that is true, all over the world. Very few countries have no gender gap, and when there is not a gender gap it's often because men know as little as women, it's not that there is an advantage there—both groups are disadvantaged, so that is not a reason to celebrate. We collected this data in January, so the findings refer to data before the crisis. There was a pandemic of financial illiteracy before the health pandemic. The level of financial literacy is very low overall, and it is even lower among women. The report shows that over time, financial literacy increases among the group that knows the most, so, between 2017 and 2020, if financial literacy increased, it's among men, not among women.

Q: What did this report find about women’s financial literacy?

A: Basically, women answered less than half of the questions we asked them. This is not a passing grade! We are very detailed in how we measure financial knowledge: we have 28 questions covering eight topics, and we measure how you can apply that knowledge so it's really a test of whether people know the basic and fundamental personal finance concepts and can apply them to the personal finance decisions we all make. The fact that women don't have a good grasp of personal finance concepts makes them financially fragile, and certainly makes them fragile entering a crisis where now financial decisions, such as managing risk and insuring against risk, are even more important. Financial literacy is critically important in a crisis like the one we are experiencing because there are so many decisions to make, for example, you need to figure out if you can postpone your credit card payments without having your credit score be affected, or whether you have put aside enough precautionary savings. The topic that women know the least—and less than men—is risk and risk management. People know the least about what is most important in this crisis.

Q: Was there anything surprising about the findings?

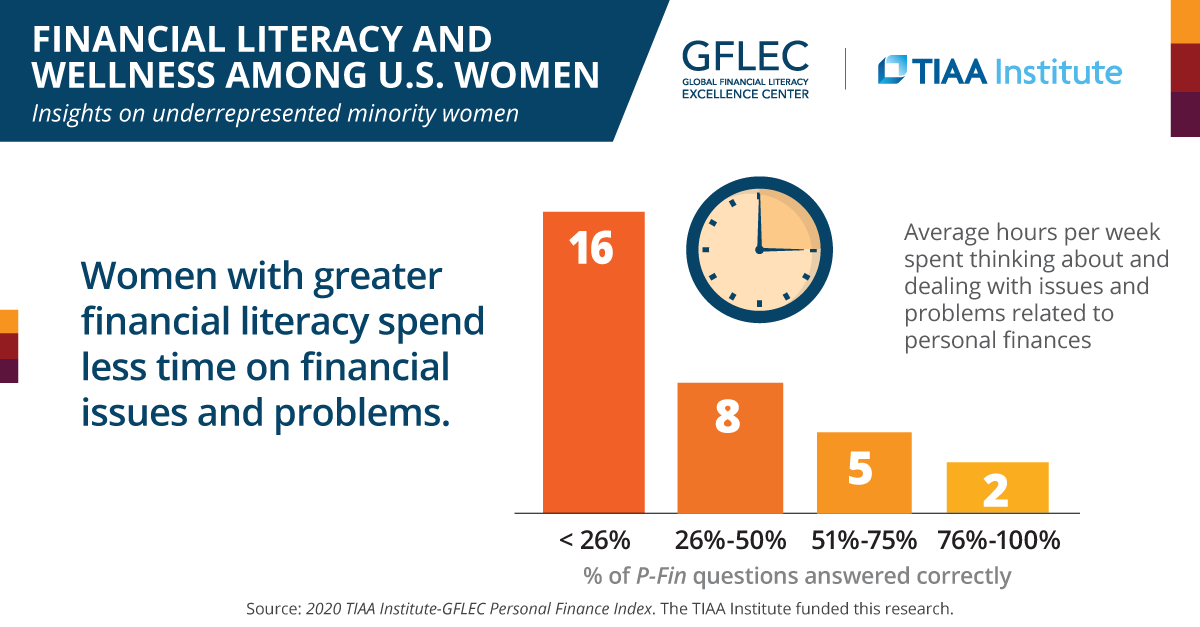

A: We asked people how many hours they spend a week dealing with personal finance issues and how many of those hours are spent at work. I expected that people probably would not give us high number (in particular the hours they spend at work) but what we found is that many hours a week are spent dealing with and worrying about personal finance. I remind you, these data refer to January 2020, when the economy was doing very well, the stock market was going up and after as many as 10 years of economic expansion. So, even when the economy was booming, people with low financial literacy were spending almost two full days dealing with their personal finance issues, often while at work. Take that number of hours, multiply by your wage, and if you are an employer you should determine if it is cost effective for you to provide financial education, because, believe me, your employees are regularly dealing with their personal finance issues. Even for individuals, if you spend so many hours on this, find a way to get advice or help.

Q: What else do these findings say about women’s preparedness for the current financial crisis?

A: Financial literacy has proven to be a shield against the shocks. We have a question in the survey that measures financial fragility, i.e., their ability to deal with shocks, and we found that women who have more financial literacy are less financially fragile. What we found is that, in January, many women would not have been able to face a small shock, let alone a big one. They didn't have the tools to deal with this, and certainly they didn't have the buffer of savings to deal with a big shock. That's also why they are the ones who suffered the most on the crisis and on top of this, we asked them to take care of children, and we asked them perhaps to decrease their hours of work —they were already fragile, and we impose on them something that made them even more fragile.

Q: What can you say about the disparate impact that Black and Hispanic women are facing due to this pandemic’s economic impact?

A: There are enormous differences across women, especially between white women and African-American and Hispanic women. The level of financial literacy is much lower among African American and Hispanic women. There is in a sense, almost a double effect on minority women, and that is something we need to address as a society, disparities are really large.

I was struck by the differences among women because and this difference is not just explained by economic circumstances. For example, it's not that because minority women have lower income or lower educational attainment. There is a gap that we need to fill. This pandemic has been cruel because it has affected the most people who had the fewest resources. I think it really speaks of the inequality that the crisis highlighted and brought about. And that's why this is a moment for change.

Q: You mentioned that you hope that people use this crisis to reimagine the future. What does that future look like to you, and what actions need to be taken to get there?

A: In finance, ignorance is not bliss. I don't know anyone, apart from Forrest Gump, who has become rich by not knowing anything about finance. One of the things we should do going forward is to make sure that there is access to financial education for everyone. People don’t learn about finance simply by watching the world around them. Moreover, it's very inefficient and very expensive to learn by mistakes. This learning should start at school. You are the CFO of your own household, and you better know something about finance because if you don't, I can assure you, and the crisis has told us, you're not going to do well. This is particularly important for women because women have potentially even less opportunities for learning. You could learn from your parents, but if your parents don't teach you because perhaps they think women shouldn't be interested in a topic like finance, then you might not learn. And if you only learn from people around you, but you spend time with children or other women who also don't know this topic, you're not going to learn a lot. I think if finance is taught in school, women are likely to benefit the most. It should be from elementary school on, starting with the tooth fairy, but it should also be in college, the average student loan for a student in the U.S. is more than $30,000. You cannot have people manage $30,000 in student loan debt if they don't know what an interest rate is. I don't have to tell you that this is very dangerous, and if you don't believe me, go and look at the 2007 and 2008 crisis.

That's why we have a personal finance course at GW. I've been teaching it since 2013, and now that I am a University Professor, I hope I can teach personal finance to any students. This course is not just about investing in the stock market. Finance is not about how to save more or borrow less or invest in the stock market—it is about the decisions that make you financially secure, that make you achieve your dreams. This is pretty good, don’t you think? Which other course teaches students how to maximize their happiness? I hope I get to teach many students next term!